What kind of insurance do I need to drive in Georgia?

Nowadays, it’s a very common question What kind of insurance do I need to drive in Georgia? Today, we will discuss car insurance coverage in Georgia. Types of Georgia’s auto insurance coverage, Georgia’s car insurance cost, the auto insurance claim process, and ways to reduce auto insurance costs in Georgia. In Georgia, third-party liability coverage is the most basic kind of auto insurance, and it is required. It shields you from having to pay for any damages to someone else’s property as the policyholder. If you cause an accident that results in someone being hurt or killed, you will also be covered.

Types of Georgia’s auto insurance coverage

To drive legally in Georgia, you must carry liability insurance. The 25/50/25 minimum coverage limits entail $25,000 for property damage, $50,000 for bodily injury per accident, and $25,000 for bodily injury per person. Just to be cautious, make sure to look for any revisions or modifications to the state’s insurance requirements!

Remember that in the event of an automobile accident, liability insurance does not cover any damage to your property or injuries to you or your passengers. If you are determined to be at fault in an accident and your damages exceed the limits of your insurance, you will be liable for the other party’s further losses and medical expenses.

We advise thinking about getting a full-coverage policy for your own car to have more complete protection. In addition to the liability, this also covers comprehensive and collision coverage.

Penalties for Driving Without Car Insurance in Georgia

State vehicle insurance laws classify driving without auto insurance as a criminal, according to the Georgia Department of Revenue. In Georgia, a misdemeanor conviction carries a possible fine of $200 to $1,000, a maximum sentence of 12 months in jail, or both. Making a false statement about your insurance coverage is regarded as a crime and is handled as a misdemeanor. According to figures from the Insurance Research Council, 12.6% of drivers nationally did not have insurance in 2019. In Georgia that same year, 12.4% of drivers were uninsured, which was slightly less than the national average.

What Happens If anyone’s Insurance Coverage Lapses in Georgia?

In Georgia, you will be subject to a reinstatement fine and receive notification from the Department of Revenue if you let your insurance coverage to lapse. Your car’s registration will be halted if the fine is not paid and no updated insurance information is submitted within 30 days. In Georgia, it is a misdemeanor to drive with a suspended registration.

Car insurance costs in Georgia

For drivers in Georgia, the least expensive minimum-coverage auto insurance policies are usually offered by Auto-Owners, USAA, Geico, Country Financial, and Georgia Farm Bureau. For a minimum-coverage insurance, all of these carriers provide rates that are less than the national average. Remember that only veterans, active duty personnel, and their families are eligible for auto coverage from USAA insurance.

| Car Insurance Provider | Average Monthly Cost | Average Monthly Cost |

| Auto-Owners | $32 | $381 |

| USAA | $42 | $501 |

| Geico | $45 | $540 |

| Country Financial | $47 | $556 |

| Georgia Farm Bureau | $49 | $585 |

Cheapest Full-Coverage Auto Insurance Rates in Georgia

The companies that often provide Georgia drivers with the lowest full-coverage insurance prices include USAA, Progressive, Auto-Owners, Geico, and Georgia Farm Bureau. For a full-coverage auto insurance policy, these suppliers usually offer prices that are significantly lower than the national average.

| Car Insurance Provider | Average Monthly Cost | Average Annual Cost |

| USAA | $101 | $1,208 |

| Geico | $104 | $1,238 |

| Auto-Owners | $109 | $1,300 |

| Georgia Farm Bureau | $119 | $1,419 |

| Progressive | $140 | $1,670 |

Optional Car Insurance Coverage in Georgia

To better protect yourself and your car, you can get supplemental auto insurance coverage in addition to Georgia’s legally minimum liability limitations. Standard forms of auto insurance to take into account are as follows:

- Comprehensive insurance

- Collision insurance

- Personal injury protection (PIP)

- Underinsured/uninsured motorist coverage

- Medical payments coverage (MedPay)

Medical payments: This coverage can provide payment for medical expenses due to injuries as a result of an accident.

Collision: Collision coverage can pay for the replacement or repairs to a vehicle after a crash.

Comprehensive insurance: This coverage offers protection from damages or losses not related to road accidents, such as theft or weather damage.

Uninsured and underinsured motorist insurance: If a driver with no insurance or not enough insurance is at fault for an accident, this coverage can cover the expenses related to the accident.

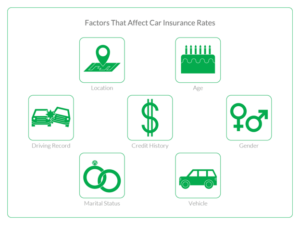

Factors That Affect Car Insurance Costs

When determining premiums, auto insurance companies take into account a number of important aspects, including:

Credit history: If your credit score is high and you have demonstrated that you are a responsible financial person, you are more likely to be awarded a lower insurance rate. Insurance premiums will frequently increase with a lower credit score.

Age: Less experienced drivers, such as young adults and teens, should budget more than older, more seasoned drivers.

Marital status: Married drivers often pay less for insurance than single motorists.

Location: The cost of your auto insurance is influenced by several factors, including the climate, population density, and even the volume of claims in your area.

Driving record: If you have a recent accident, speeding ticket or driving under the influence (DUI) violation on your record, you can expect to pay a higher insurance premium.

Vehicle type: A new car or a car that costs more to repair will often lead to a higher car insurance rate.

Gender: Men — especially young male drivers — often pay more for insurance than women.

Top Georgia Auto Insurance Recommendations

To get the best coverage for you, we advise comparing insurance quotes from several Georgian insurers. Travelers and State Farm are two excellent places to start your search.

State Farm:

State Farm is the biggest insurer in the nation, according to the National Association of Insurance Commissioners (NAIC), with 15.9% of all insurance premiums sold in 2021 coming from this company. It provides all common forms of motor insurance along with extras like payment for rental cars, roadside assistance, and benefits for travel expenses. Because of State Farm’s excellent ratings in terms of price, coverage, reputation, and customer service, we have designated it our Editor’s Choice.

Geico: Affordable for Most Drivers

Geico’s combination of affordable prices, several coverage options and strong customer service make it a smart choice for auto insurance. The company is also known for its wide selection of discounts to help policyholders save on coverage. Geico offers discounts for safe driving, new vehicles, U.S. military members and more.

Georgia is a diminished value state

Since Georgia is a diminished value state, drivers may sue the insurance carrier of the person who was at fault for diminished value. Your car loses value when it is in an accident, even if it is completely restored to its original state. Your car’s value decreases in comparison to comparable models that have not been involved in an accident. You can recover any damages you might incur when selling your vehicle by filing a decreased value claim.

You can file by getting in touch with the insurance of the person who is at fault because Georgia is one of the 15 states that provides reimbursement for loss in value. In Georgia, the following conditions must be satisfied in order to submit a diminished value claim:

- You must be not at fault for the accident

- You must provide documentation (photos, repair records, and proof of vehicle value from a trusted source)

- You must file within 4 years of the accident

- Your vehicle must have a market value of $7k+, more than $500 in property damage, low-to-normal mileage, a clean title, and be less than 10 years old

- You must have uninsured motorist coverage

What Are Mandatory Extra Coverages For Independent Insurers?

It’s critical to understand Georgia’s requirements for liability coverage. These coverages shield you from financial harm if an accident results in injuries or a lawsuit. Furthermore, supplemental insurance policies like bodily injury and uninsured motorist coverage are frequently required by independent insurers. In the case of an accident, you may make sure you’re adequately covered by realizing the significance of these coverages.

Having uninsured motorist coverage shields you from being held financially liable for the losses or injuries of another person. It usually costs about $500 per person, and drivers who drive their own cars need this coverage.

Independent insurers frequently demand add-on policies, or additional coverage, in addition to uninsured motorist coverage. Items like medical payments insurance, auto rental insurance, and property damage insurance are examples of add-on policies. Knowing how much each kind of add-on coverage costs can help you choose the one that best suits your requirements and financial situation.

ways to reduce auto insurance costs in Georgia

In Georgia, there are numerous methods to lower your insurance premiums. An agent or an online broker can help you buy insurance. You can also find out how to buy comprehensive auto insurance in Georgia without physically being in the state, as well as explore potential savings for senior citizens or active military personnel.

Please don’t hesitate to seek assistance if you need it at any point in locating suitable coverage or if you have inquiries about how your policy operates. Ultimately, drivers and those injured in collisions caused by uninsured drivers benefit from Georgia’s obligatory insurance laws.

When to Show Proof of Auto Insurance in Georgia

Sometimes you’ll have to provide documentation proving your insurance is current and satisfies Georgia’s minimal insurance requirements. It’s not always sufficient to show evidence of insurance, even though you should maintain a copy of your insurance policy card in the glove box of your car with other vital documents like your registration. Moreover, you have to be enrolled in the Georgia Electronic Insurance Compliance System (GEICS), which allows law enforcement to electronically verify your information when conducting a traffic stop. Your insurance company is in charge of registering your coverage in the GEICS.

Regardless, be sure to have your insurance card ready to show for the following situations:

- Registration transactions, such as renewals, reinstatement, and license plate changes

- At the request of a police officer

- After an accident, regardless of whose fault it is

Is Georgia a no-fault car insurance state?

No, Georgia is not a state with no-fault auto insurance. This guarantees that the driver who caused the collision will be held accountable for any injuries to other people or property damage. The first line of defense for the financial fallout from these losses or damages will be his or her liability insurance policy.

Affordable Car Insurance Rates Comparison by Cities in Georgia

For a comparison of the average monthly premiums drivers in different cities across the state pay, check out our breakdown below.

| City | Full Coverage Insurance | Liability Insurance Coverage |

| Atlanta | $173 | $65 |

| Savannah | $152 | $53 |

| Albany | $134 | $44 |

| Columbus | $140 | $47 |

| Macon | $150 | $56 |

What Types of Auto Discounts Are Available in Georgia?

If you qualify for any driver discounts, you can reduce the cost of your insurance. For instance, if you own a home and two cars, you may be able to reduce your premium by up to 25% by combining your homeowners insurance with a multi-vehicle auto policy.

Additional rate-cutting incentives consist of:

- Good driver

- Defensive driver

- Military

- Anti-theft

- Loyalty

- Good student

What’s the Best Car Insurance for Teenagers and Their Family in Georgia?

For a Georgia family with teenage drivers, a multi-car policy is typically a wise decision. Because minors are less experienced drivers, their insurance usually costs more. When you add your teen to your policy, the total amount you pay for your premium may be reduced if your insurer believes that you, your spouse, or any other adults on your policy are good drivers.

Our knowledgeable agents at Insure One assist you in locating the finest auto insurance with adaptable selections that best suit your requirements.

Alternatives to Car Insurance in Georgia

Drivers in Georgia must provide documentation of their financial obligation. The most popular way to accomplish this is to purchase an insurance policy. But there are additional methods to demonstrate fiscal prudence, such as:

- Submit a cash deposit of $100,000 to the Georgia commissioner.

- Maintain a minimum of $300,000 in investments in a bank or trust.

- Deposit a minimum of $300,000 into a savings account backed by a Federal Deposit Insurance Corp.

- Deposit a minimum of $300,000 of government bonds or notes to the Georgia commissioner.

Consequences of Driving Without Insurance in Georgia

Driving without insurance in Georgia is illegal. According to the Zebra, no insurance can lead to the following consequences:

- Up to one year in jail

- A $25 fine plus a $160 late fee if the fine is not paid within 30 days

- License suspension between 60-90 days

- Vehicle impoundment

Additional costs, including those for regaining your license or license plates, should also be anticipated. Even worse, you can be held entirely liable for any damages if you are in an accident without insurance. Georgia also verifies insurance information using a database called the Georgia Electronic Insurance Compliance System (GEICS). Even if you have proof of insurance, it needs to match the data in the system if you are pulled over.

The average cost of auto insurance in Georgia by coverage level

| Coverage Level | Avg. Monthly Cost | Avg. Annual Cost |

| State Minimum Liability Only | $42 | $504 |

| 50/100/50 Liability Only | $52 | $626 |

| 100/300/100 Liability with $500 Comp/Coll Deductible | $130 | $1,555 |

Car insurance rates by Age Group in Georgia

Drivers’ vehicle insurance prices vary according to age, with younger and teen drivers typically paying more than more seasoned drivers. The Insurance Institute for Highway Safety reports that the crash rate for young drivers is four times greater than for drivers 20 years of age and above.

Teen drivers are less experienced and more dangerous to cover, as car insurance companies are aware. Georgian drivers between the ages of 30 and 60 pay $1,526 annually on average for auto insurance, the lowest of all age groups.

See the average rates by age group below:

- For teen drivers: Teens aged 16-19 can expect to pay $6,003 per year for a full coverage car insurance policy.

- For young adults: Drivers aged 20-25 can expect to pay $2,726 a year for a full coverage policy.

- For average-aged drivers: Drivers aged 30 to 60 years can expect to pay $1,526 per year in Georgia.

- For senior drivers: Drivers age 60 and older can expect to pay $1,644 per year.

Rates based on driver profile, history and habits in Georgia

Your premiums will go up a lot if you have a history of DUIs, speeding tickets, or at-fault accidents on your driving record. Georgian drivers who are convicted of DUIs face increased insurance rates as a result of their perceived risk as reckless drivers.

Similar to this, if you receive a speeding ticket in Georgia, there’s a good possibility your auto insurance premium may go up by up to 27% when your policy renews. Generally, the first three years will cost more. Your driving history, your insurance provider, and state legislation all have an impact on your rate increase.

Here is how much your car insurance rate increases in Georgia after driving incidents:

Speeding ticket: Up to 27% increase

DUI conviction: 78% increase

At-fault accident (bodily injury and property damage): 37% increase

But even with a traffic ticket, comparison shopping can save you money.

Georgia’s regulations for auto insurance coverage are similar to those of most other states; liability insurance must cover both property damage and bodily injury. To legally drive a car in the state, drivers must fulfill these minimal standards. To offer more complete security, it’s wise to take into account extra coverage choices like collision and comprehensive insurance. The particular decision of Georgia’s auto insurance coverage ultimately comes down to personal tastes, driving styles, and necessities.

I believe if you can observe my entire blog, you may get a valid idea of car insurance coverage in Georgia . Types of Georgia’s auto insurance coverage, Georgia’s car insurance cost, Auto insurance claim process, and ways to reduce auto insurance costs in Georgia.